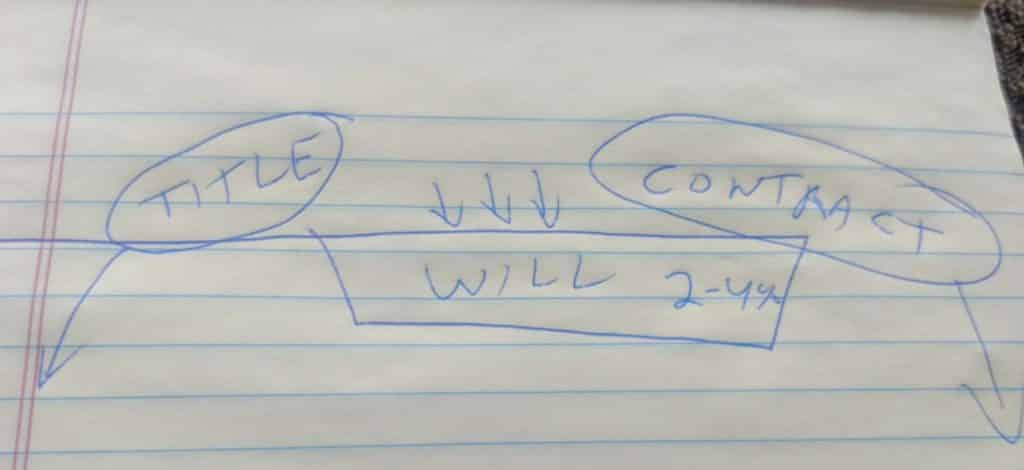

Probate is what’s left over I draw about ten frying pans a week on a legal pad. This is not due to my great artist ability. Last week I explained that Wills work through a process called Probate. When someone dies, property may be transferred by title, such as the transfer of a house to a spouse when the first spouse dies. It is easy and essentially automatic. If a person dies and the title doesn’t convey ownership, then a contract may do so instead. More about that next week. There are only three ways assets transfer at death: By Title, by Contract, or by Probate. If the title and contract don’t transfer ownership, then a probate estate does. If a decedent as a will, this is activated then: if not, then the law of the state of they lived in writes one for them. Since the dead person is not here to transfer title, that role is given to the Personal Representative. Once appointed, that person can sign contracts, deeds, tax returns, etc. All this is done with the oversight of the probate Court. Probate is not bad: it serves a necessary function. Many year ago, I was part of a bar association discussion years ago about probate and its avoidance. I was advocating the use of Revocable Living Trusts as reasonable alternatives to Court supervised transfers. I felt like a baby harp seal hunter at a PETA meeting. The outrage and venom directed at me for suggesting that Probate was to be avoided” were palpable. Most of the lawyers present, and the then Register of Wills, insisted as a strong refrain that “Probate is not that bad…” The only people I have heard insist that this is true are attorneys and Probate Court personnel. I pointed out the hypocrisy of this by position by asking “How many of you have your life insurance policies and/or retirement plans payable to their probate estates?” Of course, no one did so, because naming a beneficiary was simple and the probate Court could be avoided. If probate isn’t so bad, then why no? Maybe because of administrative fees, Court costs, Attorney fees, Personal Representative Commissions, which in Maryland can be 3.6% to 4%. Maybe because the court process can cause long delays before funds are available: from seven months to several years is not unusual. Finally Probate records are public, meaning that your neighbor can go to the Court, read your will, find out who is getting what, when they get it, and who is in control. For some of my clients, keeping this private is preferable. Is short, probate is time consuming, expensive and is completely public. The Court process provides supervision, which is some cases is badly needed. Most of my clients name people that they trust and don’t want supervised. To weigh out your options, its best to seek the advice of an estate planning attorney. Note: This is the Second of a Series of Five to be published