Should You Tell People What They Will Get?

This article discusses some of the advantages and strategic considerations of sharing estate planning details with the next generation, or “Letting the Cat Out of the Bag”

This article discusses some of the advantages and strategic considerations of sharing estate planning details with the next generation, or “Letting the Cat Out of the Bag”

While a will is one of the most important estate planning documents you can have, there are things that a will won’t cover.

Early in 2024, you should communicate with your advisers and review several items about your 2023 planning, if that planning is to have any likelihood of succeeding.

Few will argue that the most important time to have a will is when you are parents of young children.

These agents take over your affairs in specific areas, if you become physically or mentally incapacitated.

There are many stories of strange conditions in wills and trusts over time. For example, the German poet Heinrich ‘Henry’ Heine died in 1856 and left his estate to his wife, Matilda, on the condition that she remarry, so that ‘there will be at least one man to regret my death’.

This legal document can also be beneficial in many situations, such as if you want to leave an inheritance to someone but aren’t sure they will use the gift wisely.

Beneficiaries, in general, are people or entities that the holder of an account designates to receive the assets in the account, typically, in the event of the account holder’s death.

Trusts give parents of special-needs children additional options for extending care and financial assistance. However, you might need some expert help.

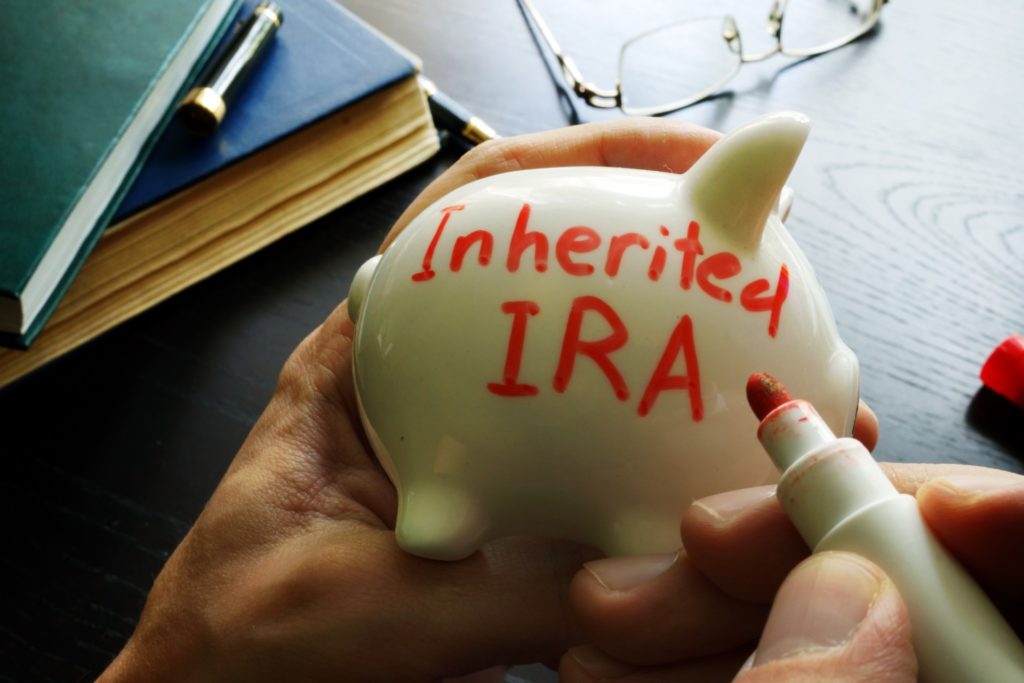

So, you inherited a retirement account. Before you make any decisions on when and how to access the money, it’s worth familiarizing yourself with the rules that apply to different beneficiaries.