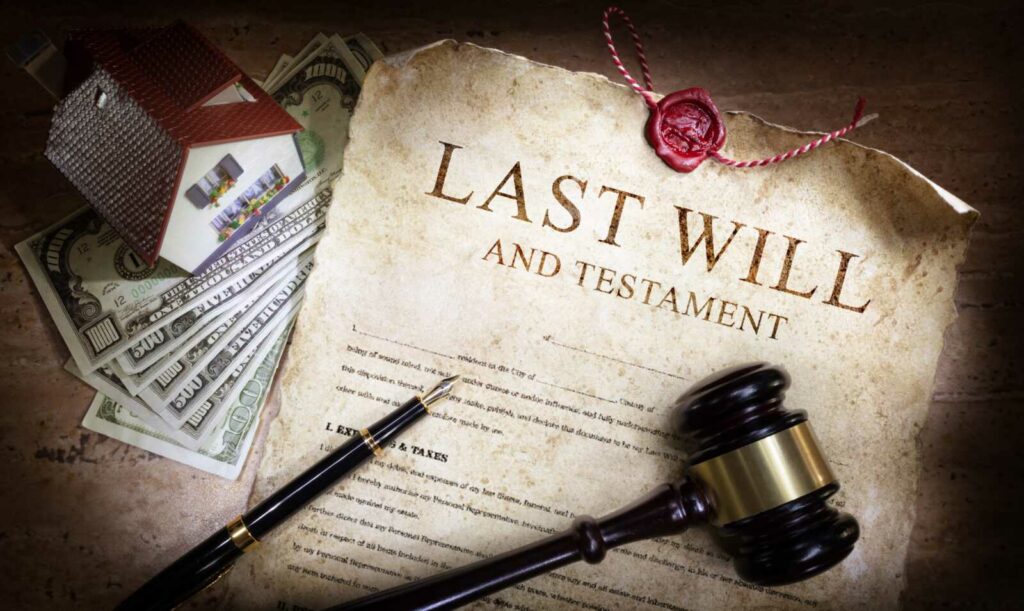

Eight Basic Executor Duties

The loss of a loved one can be an overwhelming experience. To make matters worse, there are important decisions to be made despite the grief.

The loss of a loved one can be an overwhelming experience. To make matters worse, there are important decisions to be made despite the grief.

Today’s Social Security beneficiaries may move in and out of the workforce before fully retiring. That may trigger a rule called the retirement earnings test, which can temporarily reduce benefits.

AI-driven fraud is on the rise, and that includes Social Security scams. Thieves are using artificial intelligence to get personal information that can be used to access benefits.

Even though the death of a loved one comes with unbearable grief, there are important tasks you must carry out as soon as you’re able.

The Social Security system of retirement benefits, begun in 1935, are a crucial underpinning of life for American retirees. For most people over 65, it’s undoubtedly hard to imagine life without this retirement benefit.

Knowing when to retire and when to begin claiming benefits comes down to understanding yourself — and your finances.

Even those who have saved and invested well may not be sharing their financial information with a spouse or loved one. It’s time to do that now.

In a rush to file for Social Security benefits at age 62? Many people are, but slow down and do the math first – or you might regret it.

Usually when asked to be the executor of a family member’s estate, the person feels honored and trusted. It’s a big responsibility, since the executor will be carrying out a person’s final wishes.

Here’s a closer look at the seven biggest changes to Social Security in 2021